≈

∑

∫

π

⟿

⌐

Open Source Quant Framework

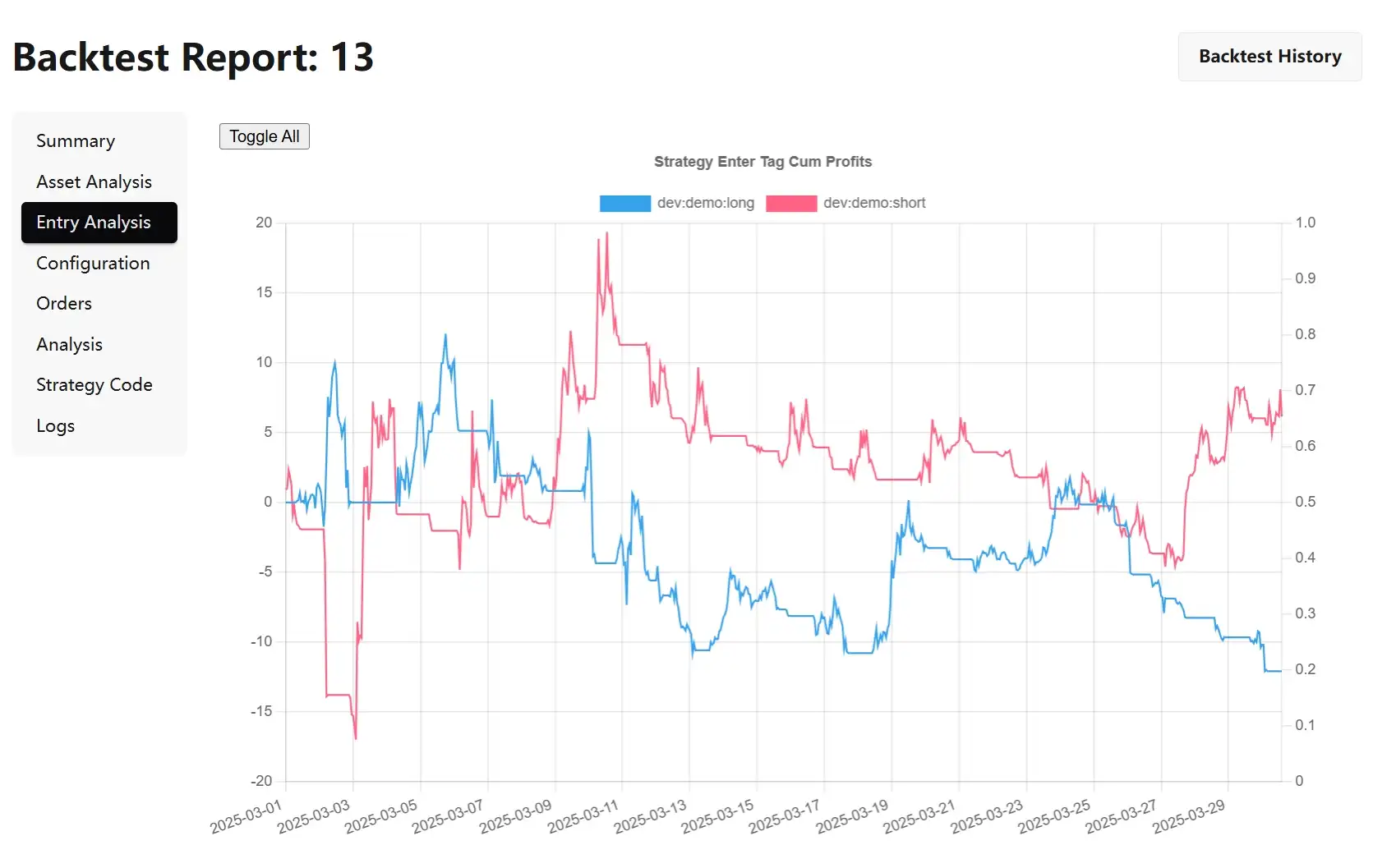

Backtest in seconds

High-performance, easy-to-use open source quantitative trading framework

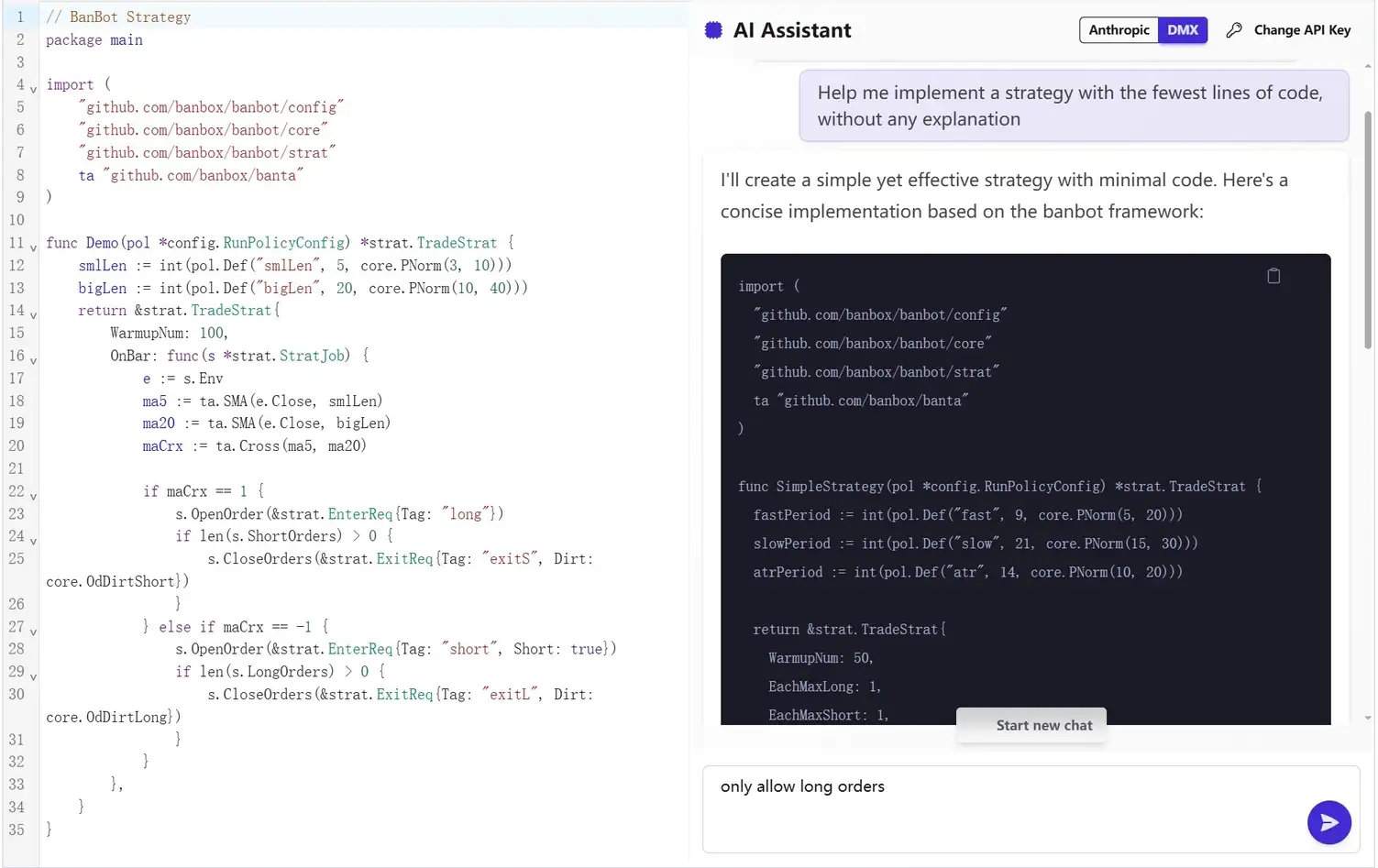

AI-Powered Strategy Reasearch

- AI-Assisted Strategy Writing •

- Get Strategy Inspiration •

- Improve Existing Strategies •

- AI-Powered Debugging •

- Better Code Understanding •

Rapid Backtesting

- • Backtest One Year of Data in One Second

- • No Lookahead Bias

- • Complete Equity Curves

- • Candlestick Order Analysis

- • Rich Performance Metrics

Hyperparameter Optimization

- Bayesian Optimization •

- Simple Syntax •

- Linear/Normal Distribution •

- Multiple Optimization Algorithms •

1 | |

2 | |

3 | |

4 | |

5 | |

6 | |

7 | |

8 | |

9 | |

10 | |

11 | |

12 | |

13 | |

14 | |

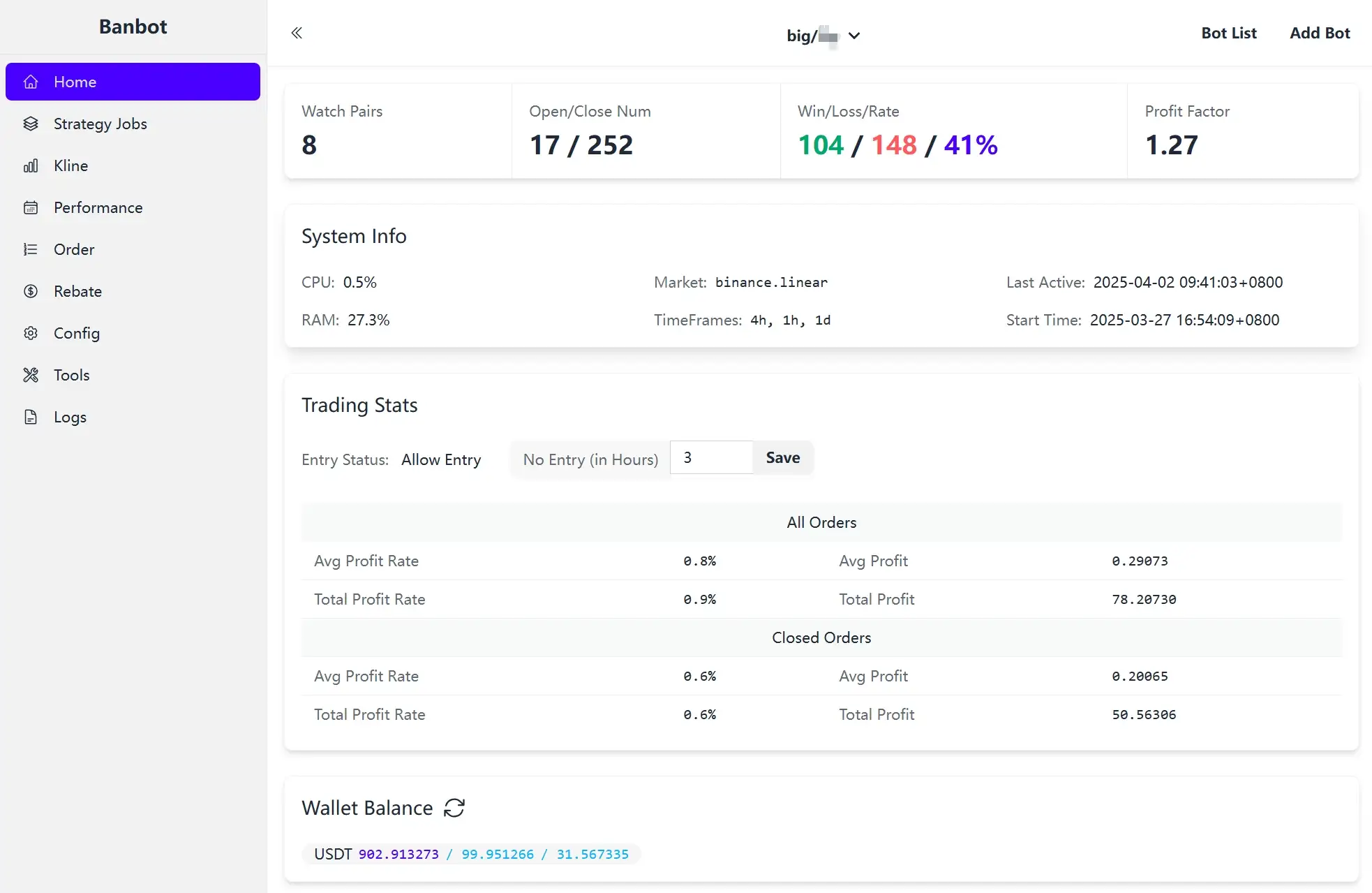

Live Trading

- • Paper Trading

- • Binance Exchange Support

- • Run Hundreds of Accounts in One Process

- • Notifications with Social Apps

- • Completely Free